(Updated April 30 to include new inflation estimates.)

Total state aid to school districts will increase by $173 million next year, or 5.3% over the current year under the bill signed by Governor Brownback last week. However, school operating budgets - the funds available for "classroom" costs such as teacher salaries, staff positions and utilities but exclude pension payments and capital expenditures - are expected to increase 1.5%, and just 1.3% on the per pupil basis.

Total state aid to school districts will increase by $173 million next year, or 5.3% over the current year under the bill signed by Governor Brownback last week. However, school operating budgets - the funds available for "classroom" costs such as teacher salaries, staff positions and utilities but exclude pension payments and capital expenditures - are expected to increase 1.5%, and just 1.3% on the per pupil basis.

That means the regular operating funding per pupil will increase, but probably not as much as the rate of which inflation, was projected to be 2.1% next year in the most recent state revenue estimates. Total funding per pupil, which includes capital costs (building and equipment) and state pension contributions, is projected to be an increase of 2.4%, but more than half of the total increase cannot be used for regular operating expenditures.

These projections reflect statewide totals. Individual district budgets will differ significantly for reasons explained below. Overall growth that is less than inflation and actual funding reductions in some districts is why many districts are already considering potential budget and personnel cuts and even though statewide total funding will increase.

These estimates were developed by KASB based on the previous estimates developed by the Kansas State Department of Education, the Division of Budget and the Legislative Research Department, revised by the appropriations provided in HB 2506 and new projections from these state agencies.

It is important to stress that these are only estimates. The actual increase in funding will be determined by how much additional local option budget authority local school boards decide to use, changes in local capital outlay use and payments on school construction bonds, and other local revenues not budgeted at the state level. Actual per pupil spending will depend on actual enrollment, which will not be known until next year.

Here is a summary of what KASB expects, based on the school finance bill.

General Funds Budgets. The foundation of the school finance system is the district general fund budget, determined by multiplying the base budget per pupil by adjusted, or weighted, enrollment. The base budget per pupil will increase by $14, to $3,852, or 0.4%. HB 2506 reduced district at-risk weighting in several areas to cut state funding by $8.2 million. At the same time, both regular and weighted enrollments are projected to increase, which means total general fund budgets will increase by $13.3 million, or 0.5%. Some districts will lose more because of cuts in at-risk weightings, while other districts will get a bigger increase because of higher enrollment growth.

Special Education Aid. State special education aid will increase slightly (0.01%) to meet estimated federal maintenance of effort requirements.

Local Option Budgets. One of the most complicated aspects of the new bill concerns the local option budget. The State Department of Education estimates that actual LOB revenues - what districts can spend - will increase by $46 million. Here is how the $46 million estimated increase was developed:

- First, the maximum LOB a district can adopt is controlled by the state. Under current law, the maximum was 31% of the district’s general fund budget plus special education state aid. Any amount over 30% required approval by district voters.

Not all districts are currently at the maximum. One reason is that the LOB is funded in two ways: local property taxes plus state aid for approximately 81% of districts, based on local property tax wealth per pupil. (The wealthiest 19% of districts in valuation per pupil do not receive state aid.) Because the state has not been fully funded the LOB state aid formula, lower wealth districts had to rely more heavily on local property taxes, which created pressure to hold down the LOB and keep mill levies in check.

Keep in mind that lower wealth districts require much higher property tax rates to raise the same amount of money as wealthy districts. That was the basis of the Supreme Court’s Gannon ruling on school finance equity. It said the state must either fully fund LOB aid or take other action to correct the “wealth-based disparities” in the LOB. KSDE indicates that fully funding LOB state aid will increase the percentage of statewide LOB authority districts would use. In other words, districts cut back on LOB use because the state wasn’t paying its share; if state aid was fully funded, districts would use more LOB because the property tax cost would be lower.

- Second, the LOB system is further complicated by the fact that since 2010, the Legislature has allowed the district’s general fund budget to be calculated for determining the LOB as if the base budget per pupil was $4,433 (the amount districts used to adopt their budgets in 2008-09), rather than actual base, which was reduced to $4,012 in 2009-10; $3,937 in 2010-11 and $3,780 in 2011-12. (It was increased to $3,838 last year and remained the same for the current year.) Without the artificial base, districts at or near the maximum percentage would have been required cut their LOB.

HB 2506 increased the actual base to $3,852 next year, an increase of $14. However, the bill also increases the artificial LOB base from $4,433 to $4,490, for the next two years only. This essentially means that districts can raise more money through their LOB without raising the percentage, because the same percentage applied to a large (artificial) base is a higher number. However, this increase is temporary.

- Third, HB 2506 changes state law to take the enrollment of students counted in virtual education programs out of the budget for determining the LOB amount. For example, if a district had 95% of its enrollment in regular “bricks and mortar” programs and 5% in on-line programs, it can now only apply its LOB percentage to the 95% of students in non-virtual programs. This will a major impact on districts with large virtual enrollment.

The impact of these changes means that districts statewide are expected to increase LOB revenue; i.e. the total they can spend, by $36 million. That assumes use of 74% of the new revenue available. However, some districts are projected to have less LOB revenue - in other words, a cut in dollars available - primarily because of the change in virtual weighting.

- A fourth change in the LOB law increases the maximum LOB amount from 31% to 33%. Any LOB level above 30% will continue to require voter approval in an election, but the new law requires that future LOB elections must be conducted by mail ballot. However, in a twist, districts that have already adopted an LOB above 30% by July 1 can adopt an additional 2% for next year without an election - but must submit the additional amount to voters for the following year. KSDE expect these districts to increase their LOB’s by about $10 million next year.

The $36 million LOB increase due to the higher artificial base and other changes, added to the $10 million LOB increase for districts already over 30%, equals the projected $46 million higher LOB spending next year. However, in order to fully fund the LOB aid formula, state LOB aid will increase about $110 million. Approximately $14 million will be required to “equalize” the additional LOB spending. The difference will be property tax reduction. In other words, because a district’s LOB is capped by the state, if state aid increases more than the LOB amount goes up, it automatically reduces the district’s LOB property tax.

Three things are important to stress.

- First, the impact on individual districts will differ significantly. Some districts will receive NO additional state aid because they are higher wealth districts. Any increase in LOB will require a higher local mill levy. Other districts will be able to raise the LOB amount and still reduce their mill levy. Still others may choose to keep the LOB at the same level and use all new state aid to reduce property taxes. The decision will be made by the local school board.

- Second, these are estimates. Districts could end up using more of the new LOB authority - or less in order to hold down property taxes.

- Third, note that a big portion of the new LOB funding may be temporary. The artificial base will drop from $4,490 to $4,433 in two years, and completely expires after three years unless the Legislature extends it. The estimated $10 million LOB increase for districts already above 30% could be rejected by voters next year.

Federal Aid. KASB includes federal aid at this point because some of these funds are available for current operating costs, such as teacher salaries. Federal aid is expected to increase $8 million next year (1.8%), with $5 million for increased free and reduced price meal payments for low income students, and $3 million for special education, Title I programs for disadvantaged students, career technical education and other programs for students and teachers.

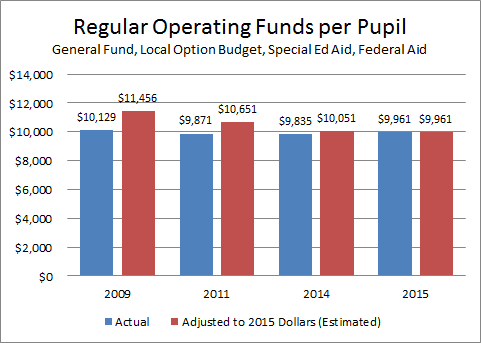

Total Operating Expenditures. These four budget areas (general fund, state special education aid, local option budgets and federal aid) represent almost all of the funding school districts can use for current expenditures like salaries, operations and maintenance. KASB estimates the statewide total next year at $4.58 billion, an increase of $67.9 million over the current year, or 1.5%. On a per pupil basis, using full time equivalent enrollment, funding is expected to increase from $9,835 to $9,961, or 1.3%.

This level would be $90, or 0.9%, higher than 2011, the first year of Governor Brownback’s administration, and $168, or 1.7%, lower than 2009, the highest level of funding before budget cuts began as a result of the Great Recession. The inflation rate, measured by the consumer price index, is projected to be nearly 8% higher than in 2011 and 13% higher than in 2009.

Capital Aid. Other parts of school district budgets have increased much more than operating expenditures. To comply with the Gannon decision, HB 2506 also includes $25.2 million to fully fund the capital outlay state aid program, which has not been funded since 2010. These funds are restricted to long-term expenditures, such as building construction, repair and remodeling, and equipment. The new law also expands use to performance uniforms and computer software. It is also possible that some districts will be able to use additional capital outlay aid to reduce transfers from other funds and free up money for general operating costs.

In addition, the bill provides $7 million more for bond and interest state aid. Both capital outlay and bond and interest aid are provided to districts with lower wealth per pupil to help finance capital costs without requiring disproportionately higher mill levies for these purposes.

In 2009, capital outlay aid was $22.3 million and bond and interest aid was $75.6 million. Next year, funding will be $25.2 million and $135 million - an increase of over 60% in these programs combined since 2009.

KPERS Funding. Another area of significant growth has been contributions for school district employees’ pensions under the Kansas Public Employees Retirement System. The contribution is based on a percentage of school district payroll for covered employees. Because the KPERS system is significantly underfunded, the Legislature has been increasing the percentage. Next year, the KPERS appropriation for school employees - which also includes employees of community and technical colleges - will increase by $37.2 million, or 10.3%, to $398 million. This amount has increased nearly 65% since 2009. Approximately 91% of the KPERS school appropriation goes to school districts and is included in district budgets.

All other revenues. The remainder of school district budgets are raised from local revenues, such as school district bond payments, local capital outlay revenues, and student fee for meals, books, activities and transportation. Because these funds are not budgeted at the state level, it is difficult to provide an accurate estimate, but for this purpose, KASB is assuming these revenues will increase 2% next year, based on comparable increases in recent years.

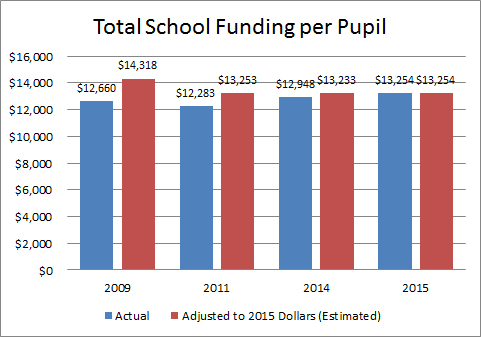

Total expenditures per pupil. Based on appropriations for capital outlay, bond and interest and KPERS funding and a 2% increase in all other revenues added to the total operating funds estimated above, KASB estimates that total school districts expenditures will increase $153.4 million, or 2.6%, next year, which would be 2.4% per pupil. This would be just slightly higher than the inflation rate projected last fall by state budget experts. However, it is important to note that less than half of that amount is for regular operating expenditures that make up 75% of district budgets statewide.

This would result in a total expenditure per pupil of $13,254, up from an estimated $12,948 in the current year. The 2015 estimate would be 4.7% higher than 2009, an increase of less than half the rate of inflation. (The consumer price index is projected to have increased 13.1% between 2009 and 2015.) The actual total expenditure per pupil will not be known until next fall when school district budgets are reported to the state.