The latest official consensus revenue estimates for the Kansas state general fund were released Nov. 10. Much of the attention has focused on a $345 million drop in expected revenues in the current year, as well projections for significant budget deficits in the next two years. KASB takes a more detailed look at how the new projections compare to longer term economic and budget trends in Kansas, and what it means for education funding.

The first part shows how Kansas personal income has consistently fallen below projections and trails the national average. The second part shows how state tax revenues have not kept up with income growth since the major income tax cuts of 2012 have decreased revenue to the state, resulting a lower percent of economic growth invested in education and public services. The third part shows how the failure of the Kansas economy to recover from the Great Recession and the failure of the tax cuts to stimulate the economy have squeezed state spending, including education.

Part 2: State tax revenue has not kept up with state personal income growth.

Part 1 of this post discussed how the Kansas economy, measured by Kansas personal income, has grown much more slowly since the Great Recession of 2008 than it has over the past 20 years, and has also lagged behind the rest of the United States. With income growth lagging, what has happened to state tax revenue?

Kansans pay two major state taxes: income taxes (both individual and corporate) and sales taxes. Most - but not all - of the revenue from these taxes goes into the state general fund (SGF). Almost all of the SGF comes from these two sources, with some additional revenue from cigarette, liquor, severance (oil and gas) taxes and insurance premiums making up about 5 percent.

The state general fund is typically about half of the state “all funds” budget. The all funds budget contains all other state revenues, most significantly, federal aid. Except for the general fund, the all funds budget revenues must be spent on specific purposes. These include all federal funds, revenues from gas taxes for highway construction, state university tuition and other income. In other words, the all funds budget includes not only taxes but fees and other revenues.

(Kansas lottery money does not go into the state general fund. It goes into something called the Economic Development Initiatives Fund and mostly spent for programs in the Department of Commerce and a few higher education and tourism programs. It does not support K-12 education and never has.)

The state general fund receives and spends general state taxes; the state all funds budget receives and spends restricted state taxes and fees and federal aid. Not included in either are local taxes raised and spent by cities, counties and, of course, school districts.

During the 1970’s, 1980’s and 1990’s, the state of Kansas took over more responsibility for many government functions, whether to provide more uniform and coordinated services, to reduce local property taxes, or both.

A good example was school finance. From mid-1970’s to the early 1990’s the School District Equalization Act used state aid to assist lower wealth districts and reduce tax rates, although the majority of school funding come from local property taxes. The 1992 school finance raised state income and sales taxes in order to increase education funding but also reduced local tax levies. For the first time, the state provided a majority a school funding.

(A more recent change concerns the 20 mill statewide school levy, which used to remain with local school districts. Starting in 2015, the 20 mill levy has been sent to the state, deposited in the “School District Finance Fund” - part of the all funds budget but not the state general fund - and then sent back to school districts as general state aid.)

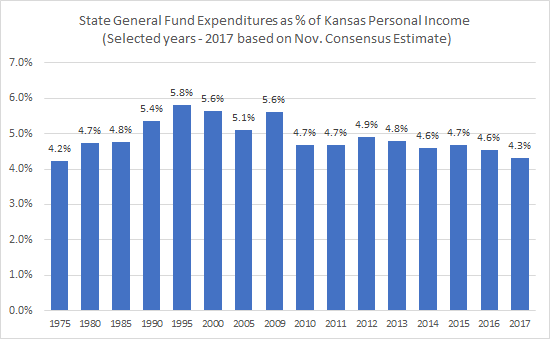

Between 1975 and 1995, when the 1992 school finance law was fully implemented, state general fund expenditures, which are mostly financed by state sales and income taxes, grew from 4.2 percent to 5.8 percent of Kansas personal income. The all funds budget, which includes the state general fund, increased proportionately, from 9.3 percent in 1973, to 12.7 percent in 1995.

Between 1994 and 2012, state general fund spending averaged 5.3 percent of Kansas personal income, and all funds spending averaged 11.9 percent.

The growth in the state general and all funds budgets did not entirely results in a higher overall tax burden (compared to personal income). A report from the Tax Foundation shows that Kansas state and local tax budget as a percent of state personal income - which would include local taxes but not state federal aid and fees such as student tuition- was 9.7 percent of personal income in 1977, 10.3 percent in 1995, and 9.5 percent in 2012 (the last year available).

In summary, state spending as a share of personal income has changed relatively little in the past 40 years, and much of the increase has been offset by lower local spending in education and other areas.

However, this relative stability began to change in 2012 when major state income tax cuts were passed. State general fund expenditures were 4.9 percent of personal income. Despite several major increases in sales and other excise taxes since then, state general expenditures have dropped to an estimated 4.5 percent of personal income in 2016.

The Legislatively approved state general fund expenditures for the current year, 2017, would drop to 4.4 percent of personal income. But if the state has to cut spending by $349.1 million to avoid a deficit, as indicated by the Legislative Research Department, expenditures would drop to 4.3 percent of personal income - the lowest level since 1976.

All funds spending has also declined, from 11.8 percent in 2012 to an estimated 11.1 percent in 2017 - and the all funds spending is inflated by over $600 million from the statewide mill levy added in 2015.

These trends are expected to continue. The new CRE expects Kansas personal income to grow at 3.9 percent in both 2017 and 2018, but projects state general fund tax revenue to grow at just 1.4 percent in 2018 and 2.2 percent in 2019. In addition, the CRE expects inflation to increase by almost 2.0 percent each of the next two years, which means state tax revenue growth won’t keep up with inflation.

In other words, not only is Kansas personal income growing at historically low rates, the current tax structure is generating a shrinking percentage of that income for state programs, such as education.

Why does this matter? It may sound good for the taxpayer to return state spending as a share of income to 1970’s levels. But are citizens willing to accept a 1970’s level of government services?

Consider some of the changes in education alone. Special education services really began in the 1970’s and costs have accelerated for children with high cost medical needs and autism. Preschool and all kindergarten have expanded to meet educational needs and parental demands. Graduation rates have increased and schools are expected to prepare far more students for college and technical programs as the share of jobs requiring advanced skills has doubled - which also has expanded the need for technical and community college and university programs.

Education at all levels is the state’s biggest expenditure, but social services are second. The cost of medical and related services today is far greater than in the 1970’s. Demands for public safety have expanded the pressure for correctional programs. Roads and infrastructure requirements have also increased.

An obvious reason for declining state revenues was the major reductions in income tax rates. However, Gov. Sam Brownback and some others have proposed shifting more of the tax burden to “consumption” taxes, which in Kansas is mainly the sales tax. But a growing share of sales transactions are exempt from tax, such as services, healthcare, and Internet sales. As a state expert explained when the November CRE was presented, people are spending more on things that are NOT taxed, and less on things that ARE taxed. As a result, the sales tax isn’t keeping up with economic growth.

Therefore, if it seems school funding and other public services are stretched more than ever and funding is not keeping up with costs and demands, it’s because it is true. Kansas has been experiencing historically low growth in its economy. At the same time, the state tax structure is providing a shrinking share of that growth for public services. For the next two years, tax revenue growth isn’t even expected to cover inflation, even with an uptick in the economy.

No comments:

Post a Comment

(Comments on this blog are moderated.)