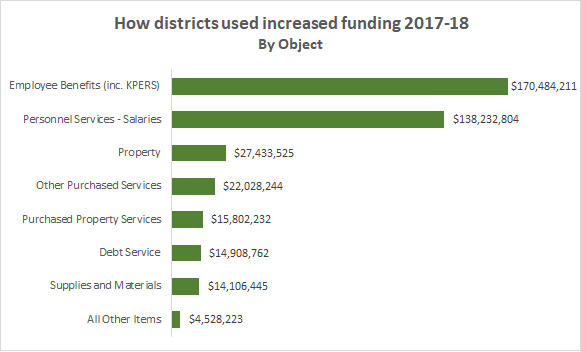

In the debate over educational funding versus tax cuts, it’s

important to understand the economic impact of state spending on K-12

education.

Data on state income levels and poverty rates show a strong

positive correlation between economic status and education levels. The same

data shows that states spending more on K-12 education have higher income

levels and lower poverty rates.

In addition, higher levels of state and local spending per

capita also have a positive correlation with higher state income. This

indicates that a low tax burden and lower spending do not promote higher

incomes and reduce poverty.

Furthermore, states that spend more on education and other

public services are

more likely to be

economically prosperous. This likely because U.S. economy increasing relies on

higher-skill employees. Investing more in education leads to a population that

is both better educated and more prosperous.

Key Points

- States with the highest average income tend to

have the highest levels of college-educated residents.

- States with the lowest poverty rates tend to

have the highest levels of college attainment

- The highest-income states tend to spend more on

K-12 education.

- States with a lower rate of taxes compared to

income are more likely to have lower incomes and higher poverty for residents

than states with higher taxes.

- Higher spending on education and other public

services supports economic growth, especially in an economy that demands higher

skilled employees.

States with the

highest average income tend to have the highest levels of college-educated residents.

There are large differences among states in average income

levels. State per capita income (total income of all residents divided by

population) in 2017 ranged from a high of about $70,000 (Connecticut) to a low

of $36,000 (Mississippi), meaning average income in the top state is almost

double that of the lowest state.

The range in the percent of persons over 24 with a four-year

college degree or higher is even greater, from a high of almost 45 percent

(Massachusetts) to a low of 20 percent (West Virginia). In other words, the

state with the highest college attainment level is more than double the lowest

state. Kansas ranks slightly above average in per capita income ($47,603, 24

th)

and well above average in college attainments (33.7 percent, 14

th).

Because persons with higher educational attainment on

average earn more than those with lower levels, it is no surprise that there is

a strong correlation between these measures at the state level. As educational

levels rise, income levels rise, with the positive correlation of almost 0.782

(the highest possible correlation is 1.0).

There are similarly strong correlations between percent of

population with four-year degrees and both median household income (income of

average household of one or more family members) and average earnings (the

average amount individuals earn from salaries and wages).

There are also positive correlations between high school

completion rates and income, but the correlation is only about half of strong,

likely reflecting the substantial additional earning power of college

attainment.

States with the lowest

poverty rates tend to have the highest levels of college attainment.

There is a strong NEGATIVE correlation between college

attainment and poverty; in other words, as college completion rates rise,

poverty rates fall.

As with per capita income, the range of state poverty rates

among all persons is quite large, from a high of 19.8 (Mississippi) to a low of

7.7 percent in New Hampshire. The Kansas poverty rate is 11.9, 30

th

in the nation, meaning 29 states have a HIGHER poverty rate than Kansas.

The chart above shows that states with fewer than 25 percent

of adults with a four-year degree or higher almost all have poverty rates of 15

percent or higher; while states with at least 35 percent of adults having a

four-year degree almost all have poverty rates below 13 percent. The

correlation is a negative 0.760. The negative correlation for high school

completion and poverty is just as strong.

The highest-income

states tend to spend more on K-12 education

Data not only show higher education levels are strongly

associated with higher incomes and lower poverty rates, it also clear that

higher education levels are almost always supported by higher per pupil funding

at the K-12 level.

In fact, the correlation between total revenue per pupil by

state in 2016, the most recent year available, and the percent of the

population with a four-year college degree in 2017 is 0.787, almost identical to

the strong positive correction between per capita personal income and college

education levels.

Per pupil funding in 2016 ranged from a high of $25,730 [SR1] (New York) to a low of $8,244 (Idaho). Kansas total per pupil funding in 2016

was $12,245 (headcount enrollment), which was 30

th in the nation,

while Kansas per capita income [SR2] was

24

th – in other words, Kansas ranks higher in per capita income than

in per pupil funding.

For example, of the 22 states that exceed the national

average in per capita income ($48,720), only four provide total revenue per

pupil of LESS than the national average for 2016 ($13,894). On the other hand,

of the 28 states below the national average in per capita income, only two

provide MORE than the national average per pupil.

Why do higher income states spend more on K-12 education? It

is almost certainly both a cause and effect. Additional educational spending

allows states to offer higher salaries to educators, promoting higher quality;

keep class sizes small to provide more individualized attention; provide more

expanded services to students such as early childhood programs, more

counselors, librarians, healthy state, school resource officers and programs to

help students, families and teachers, and improved school facilities, equipment

and technology.

At the same time, states with higher personal income can

more easily provide additional school funding. In other words, higher income

states may spend more on education in part because they have more income to

spend; but they have more income to spend because they have high educational

outcomes. Their investment in education has paid off in better economic

results; allowing them to continue making that investment.

States

with a lower rate of taxes compared to income are more likely to have lower

incomes and higher poverty for residents than states with higher taxes.

Although reducing taxes is often touted as a way to promote

state economic prosperity, the data does not support the idea that lower taxes

as a percent of income result in higher incomes and less poverty. In fact, the

reverse is true. There is a 0.304 POSITIVE correlation between higher tax

levels as a share of income; in other words, higher tax states are somewhat

more likely to have higher per capita income than lower tax states.

While this correlation is not as strong as the correlation

between education attainment and income, it certainly does not show that LOWER

taxes promote higher incomes

There is an even smaller, but also negative, correlation

(0.157) between taxes as a percent of income and poverty rates, meaning poverty

rates are slightly more likely to DECLINE as taxes rise.

Tax collections as percent of income in 2015 ranged from a

high of 16.5 percent in North Dakota to a low of 6.2 percent in Alaska. Kansas,

at 9.3 percent, was below the national average of 9.9 percent.

This data indicates that tax burden is not as significant a factor

in state income and poverty levels as educational attainment, but to the extent

it has a relationship, higher tax levels are more helpful than harmful.

Higher spending on

education and other public services supports economic growth, especially in an

economy that demands higher skilled employees.

Why do higher tax burdens have at least a somewhat stronger

association with higher incomes and less poverty than lower taxes? One reason

might be that higher spending on public services, including education, has a

positive correlation with higher incomes.

For example, total per capita state and local expenditures

(in other words, all spending by a state and its cities, counties, school

districts and other local governments, divided by population), had a 0.538

POSITIVE correlation with per capita income, and per capita spending on K-12

education had an even stronger 0.689 positive correlation. In other words, states

that spend more per capita on public services, especially education, tend to

have higher average incomes.

Total state and local expenditures per capita ranged from a

high of $19,965 (Alaska) to a low of $6,407 (Idaho). Kansas spending was $8,430,

below the national average of $9,003 and ranking 27

th.

Why does higher spending on public services have a positive

correlation with individual incomes? Likely two reasons. First, many public

goods have a positive economic impact on a state. In an increasingly knowledge-

and skill-based economy, business will expand and incomes will rise if a

state’s educational system produces more skilled residents. In addition, state

and local governments provide transportation infrastructure, law enforcement

and quality of life services that attract and retain companies and their

employees.

Second, states with higher-income residents can more easily

afford to provide these services, so they can maintain or expand them. In other

words, it is easier for high-income states to remain high-income because they

already have the advantages of a more educated population, a strong school

system and other public services. On the other hand, low-income states tend to

have a lower-skilled workforce to start with, and a lower tax base to draw on

for resources to improve education outcomes.

Lower taxes mean individuals may have more “take home” pay

in the short term, but they won’t benefit from new jobs if they lack the skills

those jobs require; and higher paying jobs are more likely to move to a state with

a workforce that has the educational levels to fill them.