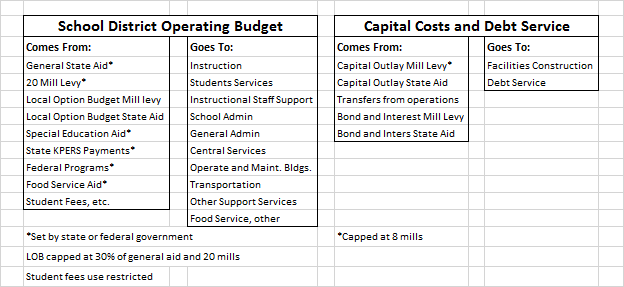

School spending is divided into two areas. The first, general operating expenditures, go to salaries, utilities and materials. The total amount of these funds is mostly limited by the state and federal governments, however, local boards decide how to spend what they receive.

The second, capital expenditures and debt payments go to acquire, build and equip facilities and pay for constructional bonds. The amount of these funds are mostly controlled by local school boards and voters. However, these funds can only be used for building costs and limited use for building maintenance.

As noted in the chart, most operating funds are set by the state or are based on federal appropriations. Districts may adopt a local option budget for operations, but the amount is capped at 30 percent of the general fund, which is set by the state Legislature (or 33 percent if the district holds an election).

Follow-up: Why do school districts spend money on buildings and other facilities when they are concerned about operating costs?

The amount of funding for general operating costs is set by the state. Many districts have reached the state imposed limit on what they can raise for local option budgets. However, districts can raise up to eight mills in local property taxes for building construction, upkeep and maintenance; and there is no limit on what local voters can approve for construction bonds. The dollars raised for facilities cannot be used for most salaries and operations even if the board would prefer.

No comments:

Post a Comment

(Comments on this blog are moderated.)